Good Pools and Bad Pools on Uniswap V3

Why are some pools good 🐶 and other pools bad 😈?

The answer comes from breaking down LP profits into:

- Price changes 📈

- Fees collected 🎟️

By comparing LPs to options, we discover parallel insights — let's explore!

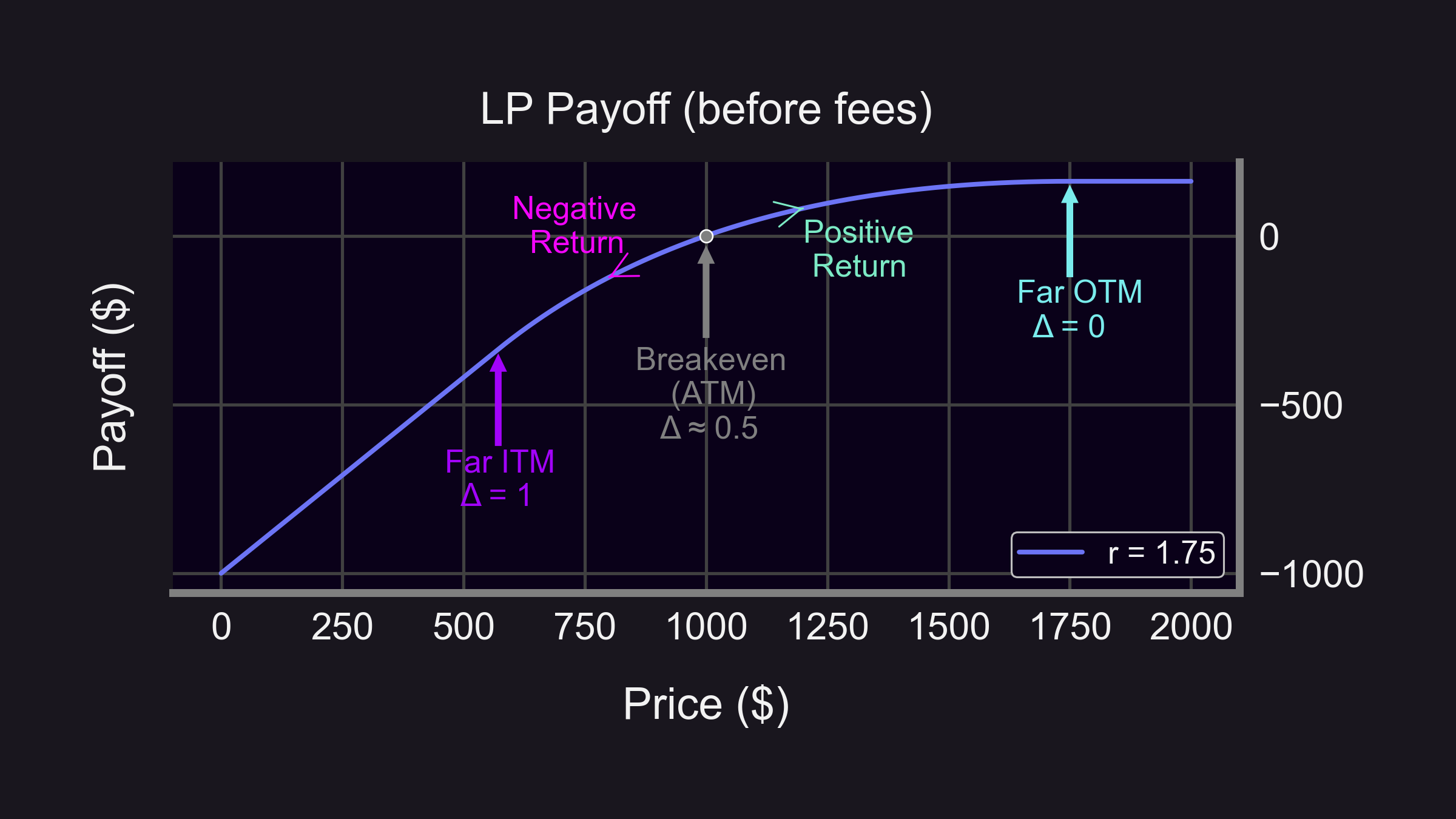

Price changes

- ⬆️ Price up: positive return

- ⬇️ Price down: negative return

- ⤵️ Payoff determined by delta (Δ) & gamma (Γ) of LP position

Why use options terminology (Δ & Γ) for LPs? Hint: that payoff looks awfully like a short put option!

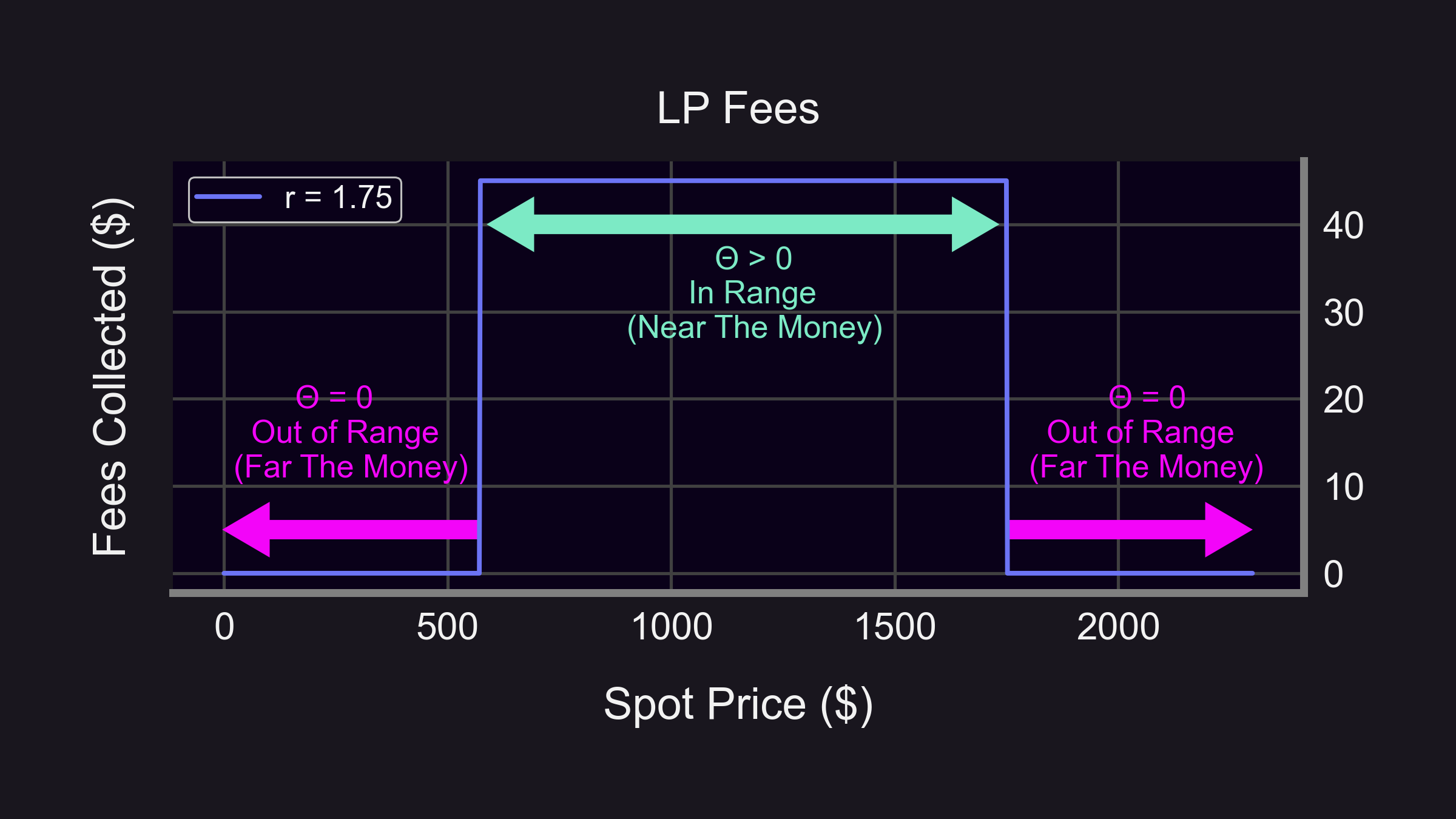

Fees collected

Fees collected are determined by the theta (Θ) of the LP position.

🕒 Θ: Rate of time decay (dV/dτ)

💰 dV = fees collected

🧊 dτ = 1 block → Θ = fees per block 🤯

✅ Near the money: Θ > 0

❌ Far the money: Θ = 0

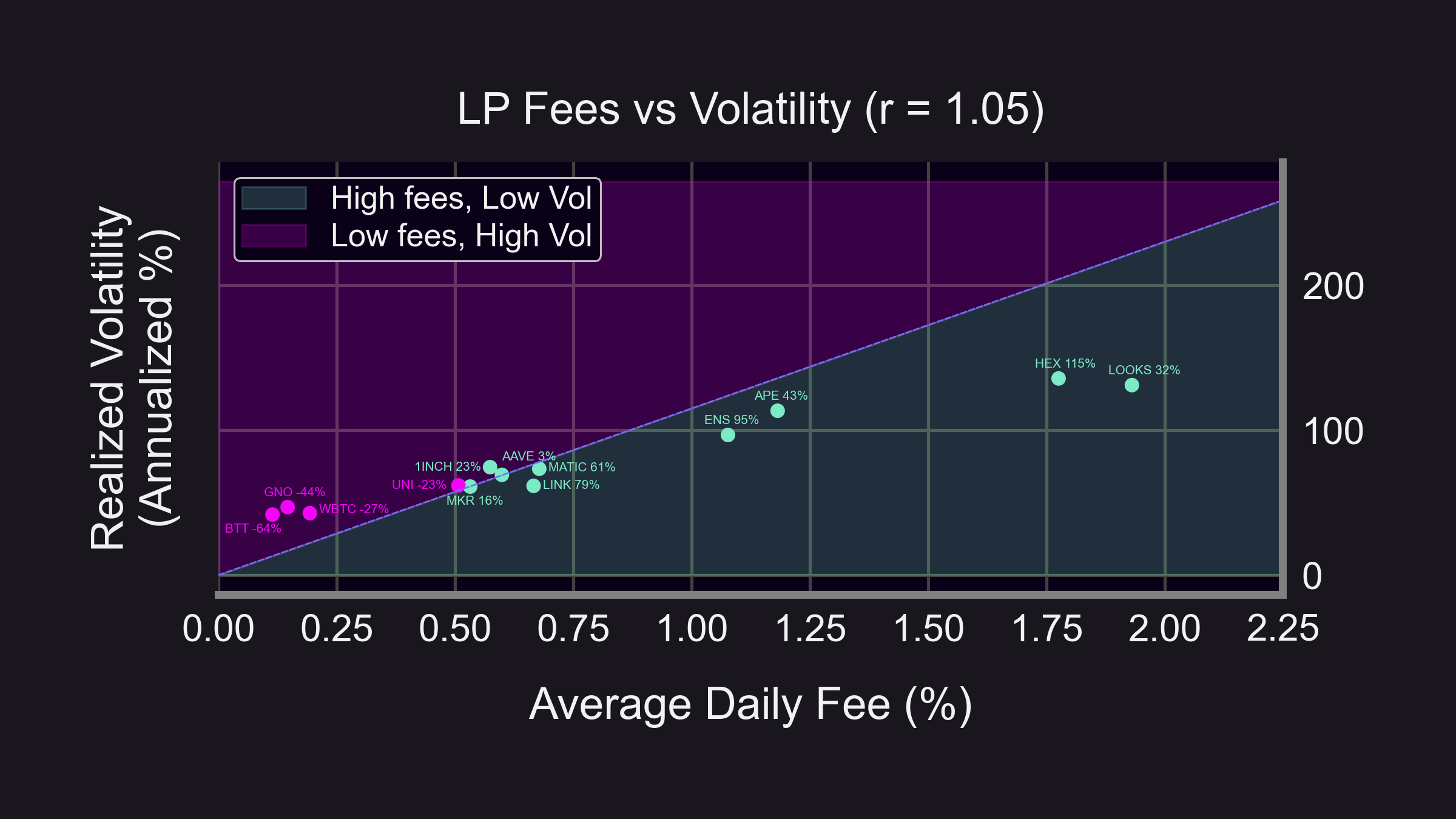

Implied Volatility vs. Realized Volatility

In TradFi, options selling is more profitable when Implied Volatility (IV) > Realized Volatility (RV). Can we compare IV-RV for LPs?

Yes! But let's use fees instead of IVs since:

- Easier calculation 🧮

- Fees collected ⇔ options premia 👇

- ⬆️ options premia ⇔ ⬆️ IV

Results match TradFi! 👇

- 🐶 Good pools (green dots): lie below the line, compensated by high fees given volatility ("IV > RV")

- 😈 Bad pools (pink dots): lie above the line, not compensated enough ("IV < RV")

(Dot values are summed returns from LPing)

How do price changes and fees affect returns?

- ⬆️ Price → ⬆️ LP returns (since fees are always positive)

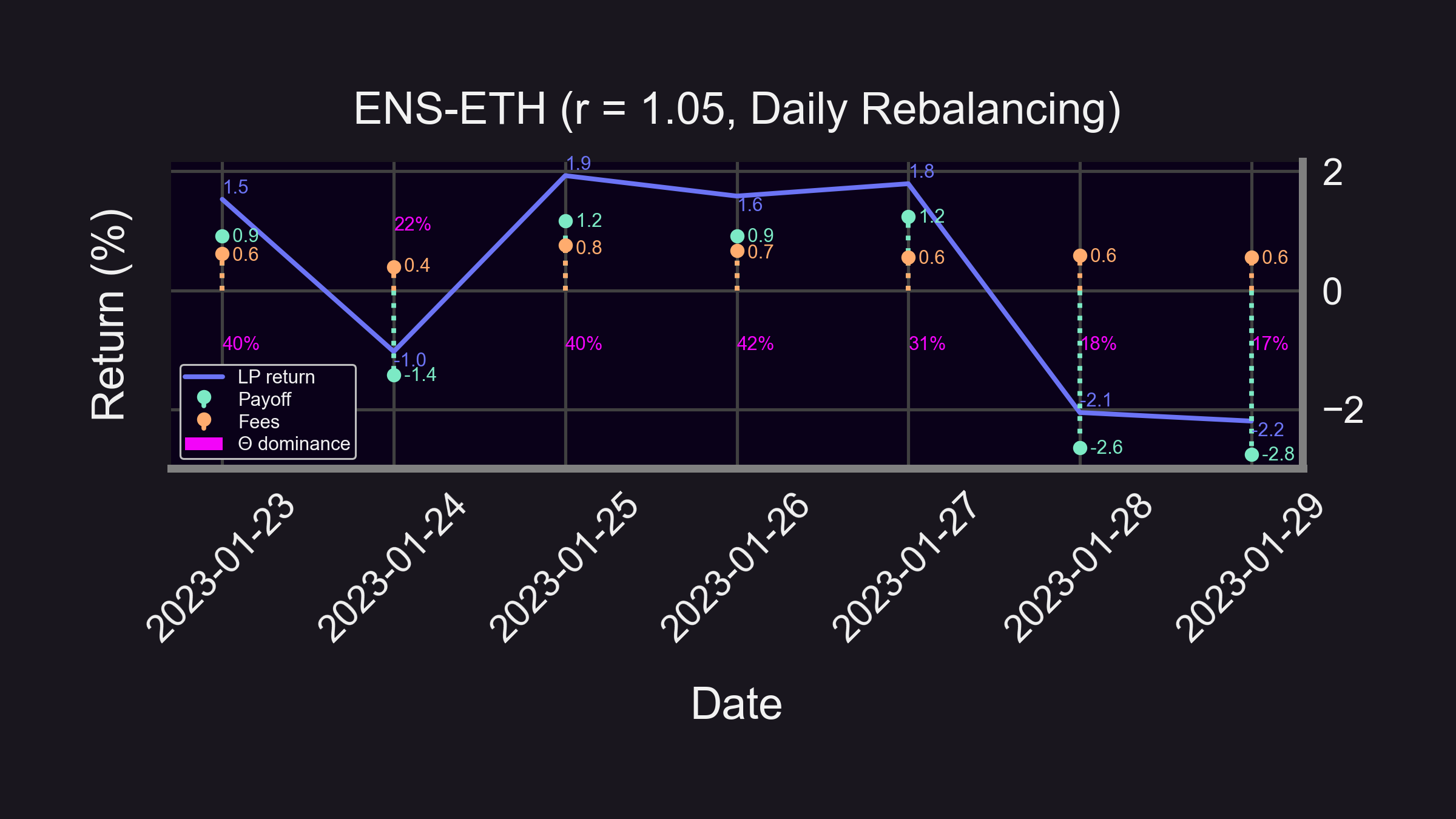

- ⬇️ Price → ⬆️ LP returns if Θ dominates

- ⬇️ Price → ⬇️ LP returns if Δ & Γ dominate

Let's define "dominance" so we can analyze pool returns! 👇

We define a metric to measure how much fees dominated LP returns:

(fees & payoff expressed as percentages)

Meaning:

- 💪 100% Θ dominance → fees drove 100% of LP returns

- 🤕 0% Θ dominance → price movement drove 100% of LP returns

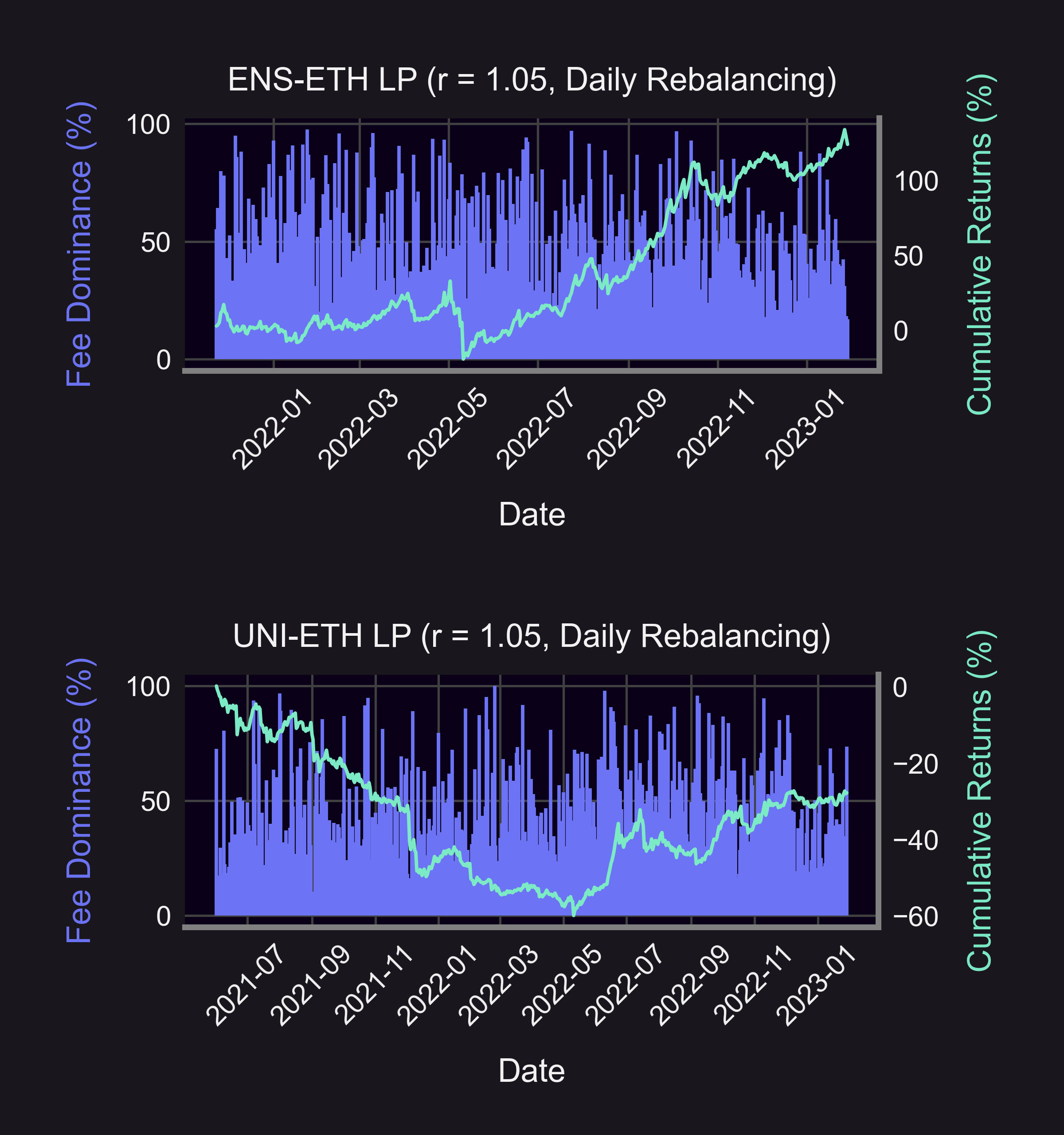

Previously, we found that LPing on ENS was highly profitable (+124%), but UNI was not (-28%). By graphing Θ dominance next to cumulative returns, we find:

- 😔 Bad days (negative returns) driven by price movement

- 🥳 Good days (positive returns) driven by fees

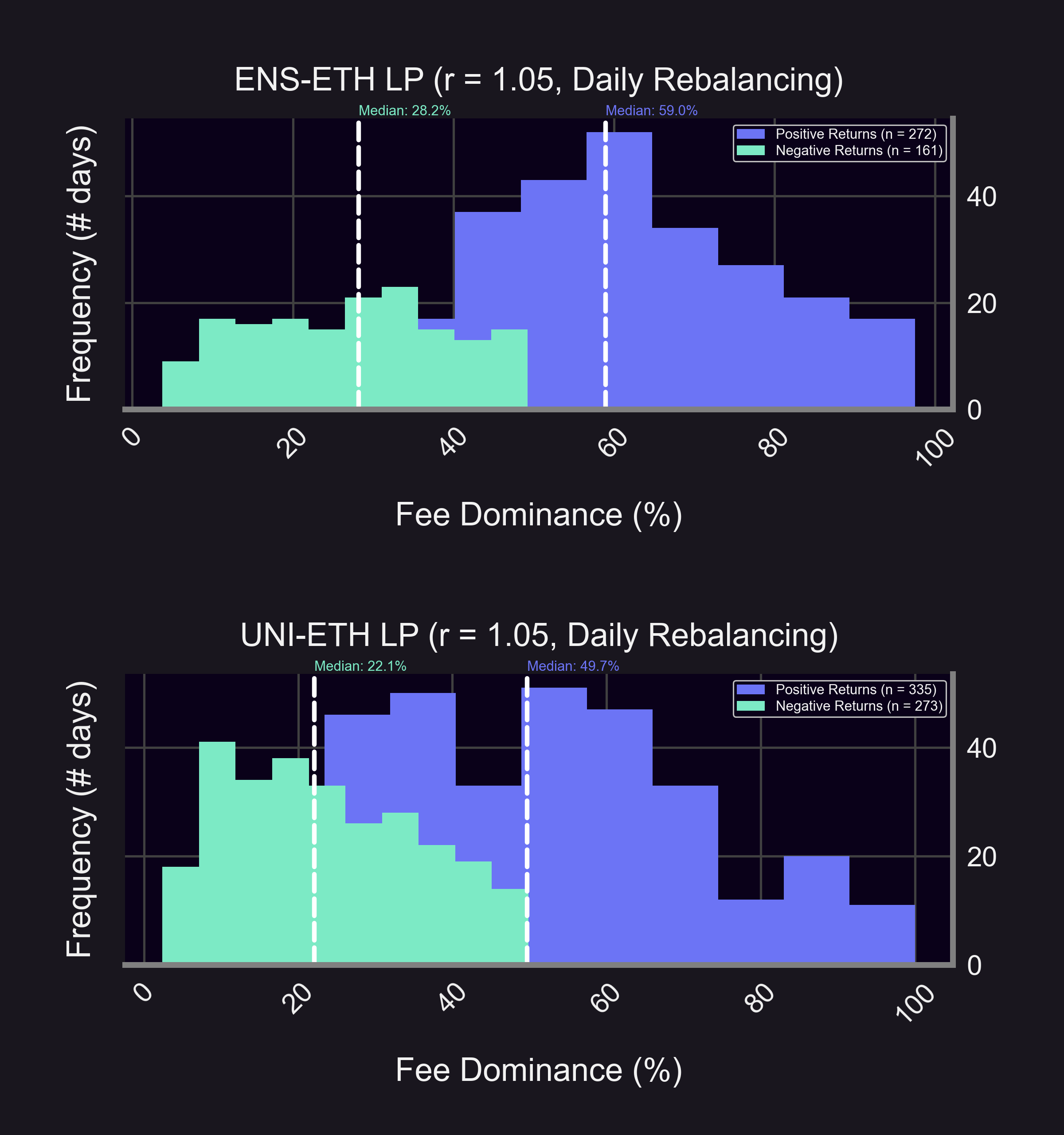

Breakdown of positive & negative returns confirms that good pool Θ dominance > bad pool Θ dominance:

- 😔Bad days: 28% (ENS) > 22% (UNI)

- 😊Good days: 59% (ENS) > 50% (UNI)

The good pool also had a higher proportion of good days:

- 🤩ENS: 63% (272/433)

- ☹️UNI: 55% (335/608)

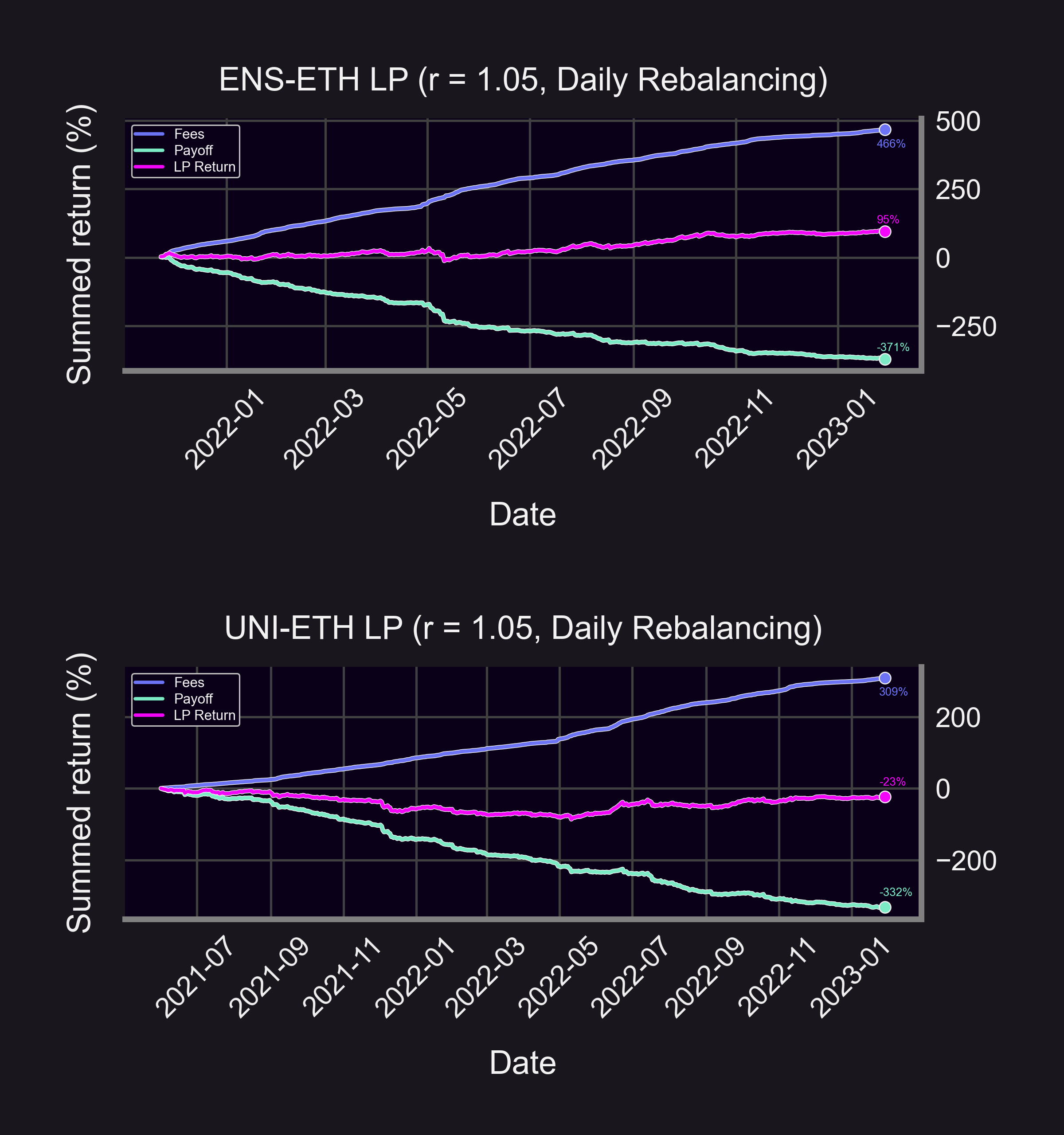

The good pool's fees made up for its bad payoffs (ENS):

- Fees: 466%

- Payoff: -371%

- Return: 95%

The bad pool's fees weren't enough to compensate (UNI):

- Fees: 309%

- Payoff: -332%

- Return: -23%

(All values are summed)

Summary

📣 Key Insights:

- LP = short option payoff

- Δ, Γ, and Θ affect LP returns

- LPs compensated when IV > RV

- Good days/pools driven more by fees than by price changes

Disclaimer:

- 📢 None of this should be taken as financial advice.

- ⚠️ Past performance is no guarantee of future results!